The Cedi’s Sudden Rise

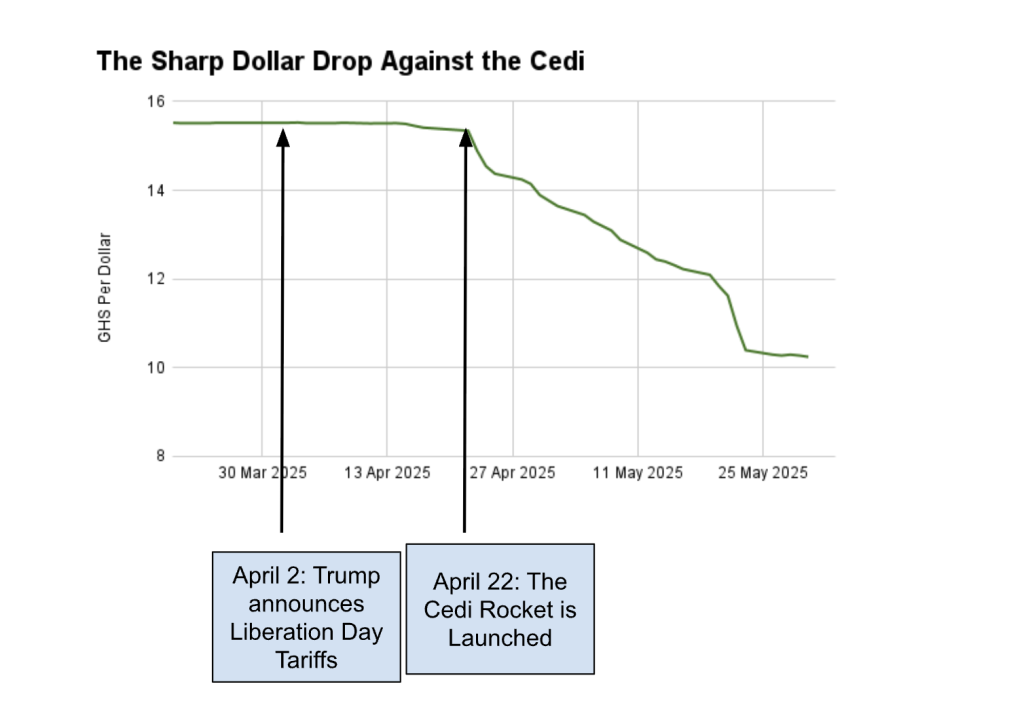

In the middle of April 2025, after what seemed like an endless fall against the US dollar, the cedi pivoted and as if launched by an invigorated invisible hand, began a surprising rise. By the end of April, it had increased from $0.0645 (i.e. 15.50 ghs/$) to $0.0707 (i.e. 14.14 ghs/$) – a 9.6% increase in the value of the cedi! With its renewed wings, the cedi continued to soar till it reached $0.0974 (10.27 ghs/$) by end of May. The fury with which the cedi has appreciated has stoked suspicions and wonder in Ghanaians, who although excited about their currency’s recent glory, remain anxious about its durability. In this article, I will explain why the suspicions of the Ghanaian are warranted and offer the Government a more credible proposal to maintain cedi’s stability.

The Cedi’s Long Losing Battle with the Dollar Makes Its Recent Rise A Shock

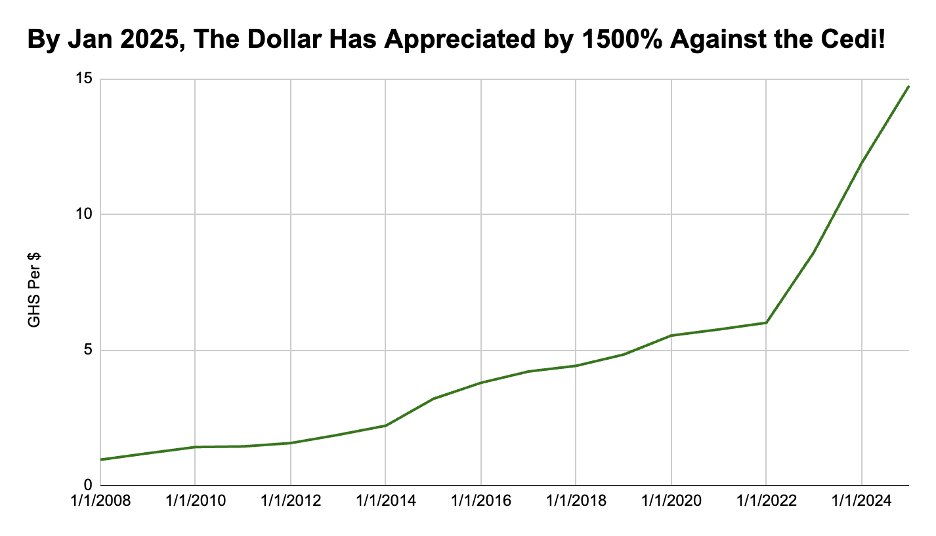

In 2008, the Ghanaian currency gained parity with the US dollar. The parity was not achieved by a positive development of the country’s trade balances or any significant changes in the structure of the economy; it was achieved by merely redenominating the currency: 10,000 of the old currency was now 1 GHS (new currency)! Therefore, while a dollar was worth about 9500 old cedis before the redonomination, it was worth, thanks to the power of merely slashing off zeros, 0.95 GHS. Although this was a cheap exchange rate success, Ghanaians nevertheless celebrated the superficial equality of their currency with the most powerful currency in the world. Our pride was however short-lived!

By January 2014–within merely six years of redonomination–the dollar had more than doubled in its relative value against the cedi (220% cumulatively, 14% annually). The dollar would continue to appreciate at about 13% per annum for the next eight years (2014-2022) to be about six times its value at the time of redenomination. Then for the next three years (2022-2025), the dollar would increase by a whopping annual rate of 35% against the cedi and skyrocket to almost 15 times its value as of redenomination! This sure domination of the dollar over the redenominated cedi over its entire lifetime makes the cedi’s recent sudden palpable recovery against the dollar mysterious.

What then underpins the cedi’s sudden rise? Many experts including the current governor of the Bank of Ghana have alluded to the general depreciation of the dollar against all currencies and the sharp appreciation of Gold, both of which were facilitated if not sparked by Trump’s declaration of tariffs on the world on April 2, 2025, a day dubbed as Liberation Day. I shall explore each of these factors and whether they fully account for the cedi’s new glory

The General Depreciation of the Dollar Does Not Fully Explain the Cedi’s Rise

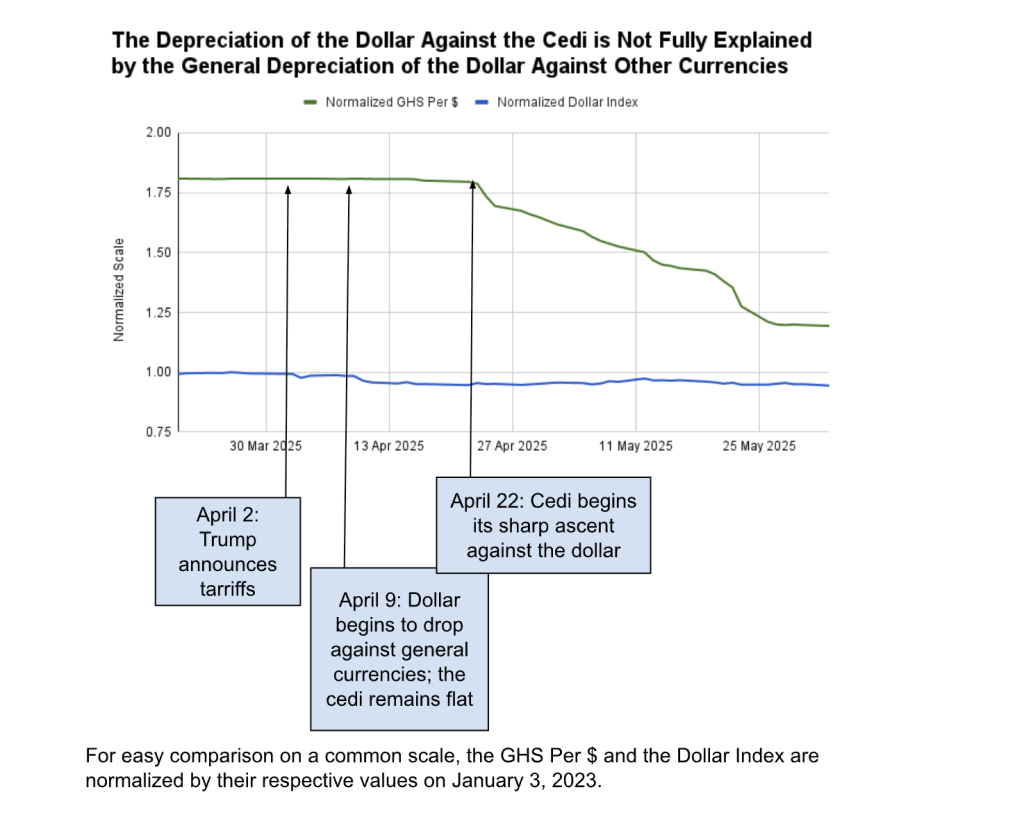

On April 2 2025, a day dubbed ironically as Liberation Day, President Trump declared tariffs on all imports to the United States.Since that declaration, the dollar began to steadily decline against most world currencies, losing about 4.2% of its value on Liberation Day by the end of April. It’s attributed that investors, angered by Trump’s unprovoked trade war, moved their assets away from American securities to challenge America’s complacency with its exceptionalism and powers. It surprisingly took about three weeks after Liberation Day for the cedi to appreciate against the dollar. Why it took that long is still an economic mystery to unravel. However, when the cedi finally began to appreciate, it appreciated with an unprecedented fury! The cedi began its sudden sharp ascent on April 22, 2025; by the end of April–just after 8 days–it had risen by about 9%, more than double the rate at which the dollar had depreciated against other major currencies. But as drastic as the rise was, the cedi was not done with its flight up. By the end of May–within just five weeks of its ascent on April 22– it had cumulatively appreciated by a whopping 50%!

Clearly, the general weakening of the dollar (4.2%) cannot account for even a tenth of the magnitude of the cedi’s sudden rise. One of two things can therefore be true: There was a windfall increase in our import reserves due to rising gold prices which caused such a sudden rise in the cedi. Otherwise, Ghana’s central bank–Bank of Ghana–may have suddenly realized that the cedi had long been grossly undervalued and hence instituted a punctuated correction. Only the Bank of Ghana can attest to the latter; however, I will investigate the former by assessing whether the recent increase in the price of Gold can explain the phenomenon.

Gold Does Not Explain the Cedi’s Rise Neither

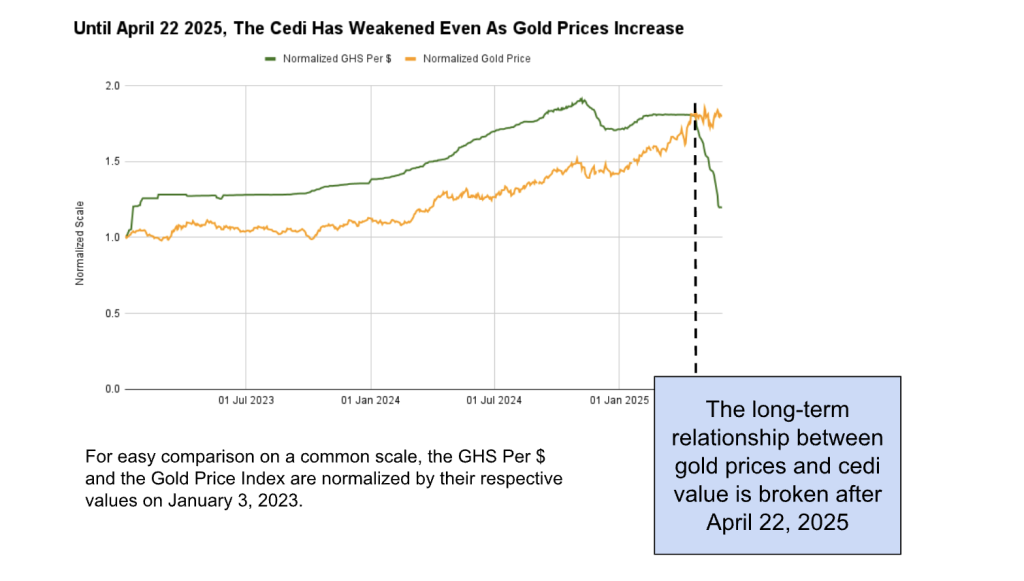

Gold is a strategic asset in Ghana’s foreign exchange portfolio and has been leveraged in diverse ways in the nation’s foreign exchange management. In late 2022, to deal with the exchange rate crisis, the ruling NPP government introduced a Gold-for-Oil program in which it paid for oil imports with gold bars. The current NDC government has scrapped the program and replaced it with a GoldBoard charged with a centralized mandate to trade gold for the benefit of the nation. Despite how Gold has been critical in our foreign exchange strategy, the cedi, as seen in the chart below and until April 22, has historically depreciated even as Gold prices rose. One would think that as a nation of gold, rising gold prices would have rather helped improve our trade balance terms and hence our currency.

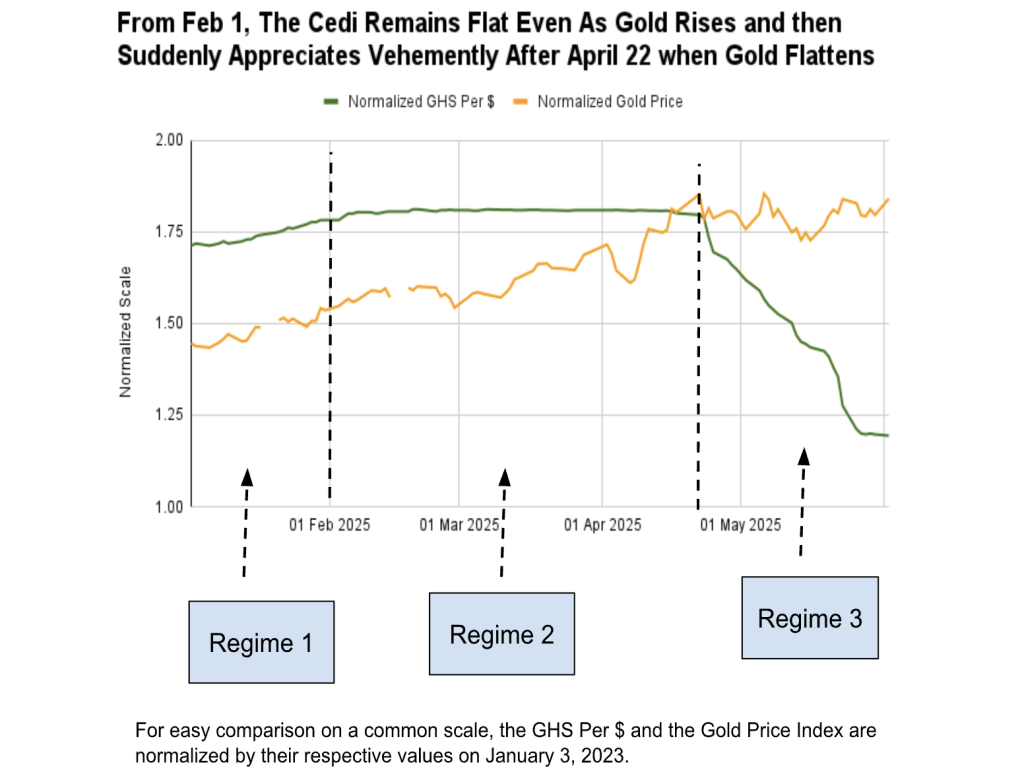

Even more surprising than the negative correlation between the cedi’s strength and gold prices is the sudden big drop of the dollar against the cedi on April 22. By April 22, gold had cumulatively increased by about 85% while the dollar had also appreciated against the cedi by 80% as compared to their respective values on January 1, 2023. However, this long-term negative covariation between the value of the cedi and the price of gold would magically reverse on April 22, when the cedi unprecedentedly rose (and sharply) even as gold prices flattened! To see this aberration more clearly, it’s worth studying the covariation between the cedi and gold from the beginning of this year.

The three regimes demarcated in the chart below show three patterns of covariation. The first regime (January 1 – February 1) shows the usual historic pattern of the cedi depreciating even as gold prices rise. The second regime (Feb 1 – April 22) shows a somewhat surprising flattening of the cedi even as gold prices continue to rise; and the third regime shows a bizarre covariation where the cedi appreciates vehemently even as gold prices remain flat.

It’s really not clear why the cedi would remain flat during regime 2 even as gold rises but then suddenly appreciates as if with some pent up vengeance when gold prices have stabilized. The nonsensical pattern speaks of a visible hand that has deliberately taken over the invisible hand of the exchange rate market to direct it to wherever it–the visible hand–desires! It also speaks of a central bank who lacks a sophisticated evidence-based framework to determine exchange rate using relevant market variables and therefore leaves the market amenable to the adhoc vicissitudes of the Governor’s sentiments.

The Economic Fundamentals Do Not Explain the Cedi’s Rise

The state of the economy described by the Finance Minister, Dr. Ato Forson, in the March 11, 2025 budget statement is not one that can engineer such a sudden big rise of the cedi within such a short timespan! Ghana is saddled with high debts (about 61% of GDP); one ought to just read lines 73-85 of the March 11 2025 budget to catch a glimpse of debt pressures pulverizing our nation. Even the minimal reductions we’ve seen in our debt levels since 2023 have been achieved through harsh haircuts, debt restructuring and graces from our debtors rather than us making direct payments. External financing remains frozen and the government gets majority of its funds from domestic sources. It’s not farfetched that the government may have actually orchestrated this low value of the dollar so they can buy them cheap to pay their mountains of external debts which are quickly coming due–a more subtle way of passing the pains of the debts to the Ghanaian people. The economy remains mildly industrialized and relies on the rest of the world for most of its manufactured goods. Unemployment and inflation remain elevated and are beyond what is healthy. Cocoa Board–the agency that runs one of our chief export commodities–and ECG–our chief energy custodian– are in crisis. It’s therefore hard to believe that such an economy described euphemistically by the Finance Minister as “precarious” (see line 63 in March 11 2025 budget statement) suddenly has any umph to move even a feather let alone the cedi against the strongest world currency by a whopping 50%!

Mahama’s Exchange Rate Chimera: A Floating Rate System With A Fixing Hand!

After April 22, 2025, when the exchange rate began to skyrocket, many began to ask the Bank of Ghana for explanations. This article has now proved with convincing data and economic reasoning that all of the reasons given by the authorities are phony and fail to explain the rise. Yes the dollar dropped but only about just 5% (not 50%) even against the major world currencies. Yes gold prices rose but historically, such increases have actually weakened and not strengthened the cedi; the best effect a rising gold price has had on the cedi in recent history is to have no effect at all; hence for gold to have suddenly caused the cedi to appreciate by as much as 50% sounds mysterious. And lastly, the structural problems of our economy remain dire as attested to by the Finance Minister. President Mahama has been in office for just about four months. It’s incredible that he’s done anything substantial within his short reign to organically change the gravitational course of the exchange rate. It is therefore reasonable to suspect that the 50% dollar drop against the cedi is man-made even as the government and the central bank insist that our exchange rates are floating and follow the orders of the market!

I am a big proponent of the market system as I believe that no person or group of people no matter how smart can be intelligent enough to manually dictate and pilot the market for the optimal welfare of its participants. And even, such an elite group given that much authority will likely abuse it for their own greedy benefits. It’s well understood in economics that such centrally-planned economies result in painful market distortions, dwindled producer and consumer surpluses, shortages and other distasteful outcomes. The best known determinant of price are the market participants themselves who willingly express their desires to buy and sell, and through such free expressions of demand and supply, they collectively determine the market price that will maximize their collective surplus.

There’s also evidence that the central bank lacks a sophisticated exchange rate framework or model that leverages market-based factors to derive an exchange rate that achieves a pre-specified set of meaningful macroeconomic targets or goals such as exchange rate stability, forex reserve protections or any other deemed worthy by the central bank and its stakeholders. This can partly explain why our import reserves have bounced around erratically and our currency has been more volatile than necessary. The lack of an exchange rate framework or model also makes it hard for market participants to derive useful forecasting models to make inferences about exchange rate trajectory and consequently worsen the macroeconomic uncertainties. There can therefore be few investments worthier than the development of such a framework.

Leave a Reply